Appraisal or Inspection: Which Do You Need?

East Coast Appraisal Service • May 24, 2023

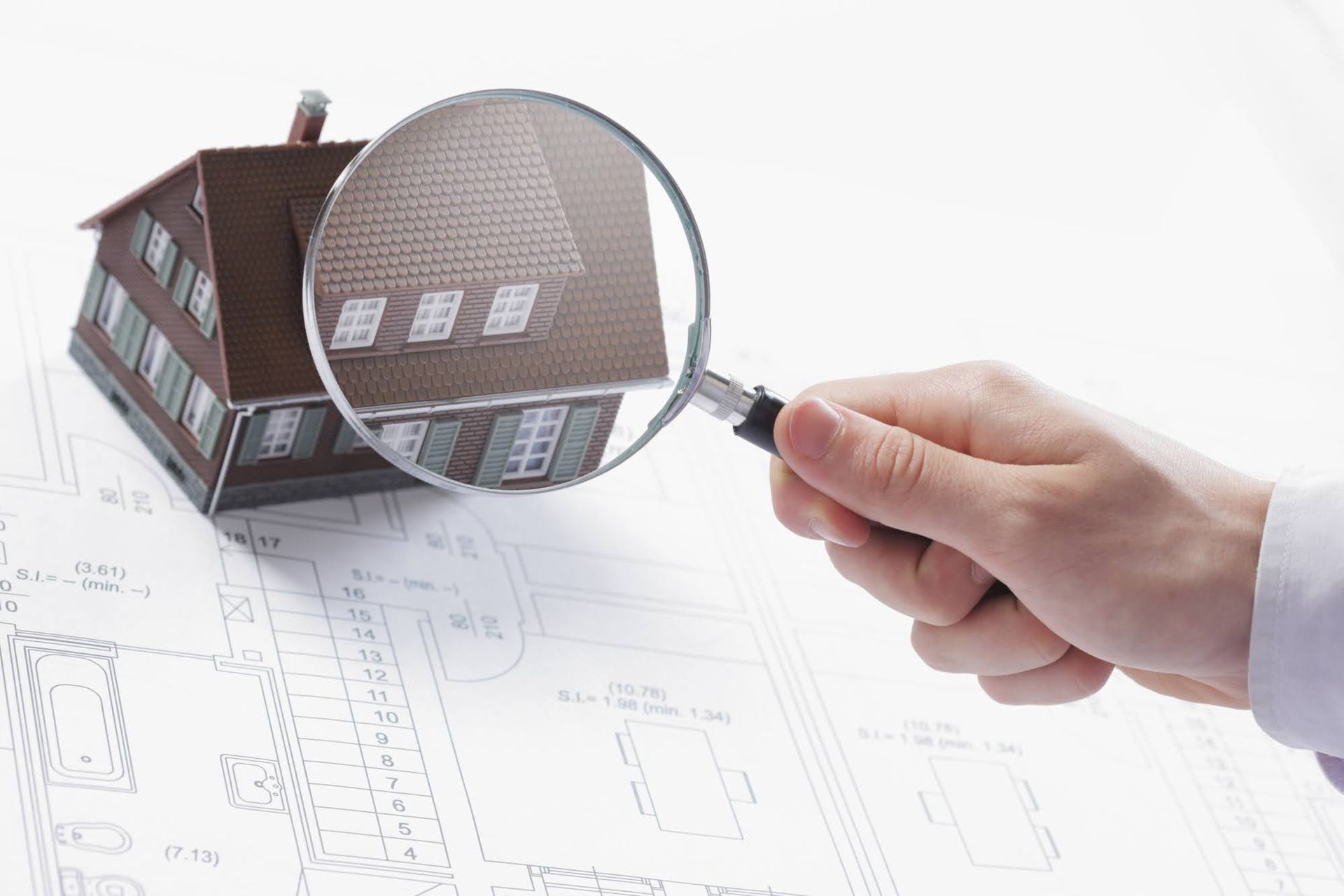

While trying to buy a home, you may have found out that some lenders require their borrowers to have an appraisal and/or an inspection completed. Some lenders may only require an appraisal and leave the decision about an inspection up to you. Because of this, it is important to know the differences between the two.

Home appraisals are often required by a lender for the initial purchase or refinancing of a home. Home appraisals are a way to determine the value of the home. A lender will not borrow you more money to purchase a home than it is appraised to be worth.

Though an appraisal is usually required by the lender, the borrower (home buyer) is usually responsible for paying for the appraisal. There are times when the seller could pay for the cost of the appraisal, but that is a deal that needs to be worked out through your real estate agents as it is not typically the seller's responsibility. Home appraisals cost around $300 to $450 so make sure to account for that cost when you are saving to buy a home.

To keep it fair, there are regulations in place that require an appraiser to have no connection to the seller and the buyer. This prevents a buyer or seller from having the ability to call in a family member to give a biased appraisal and say that the house is worth more/less than it actually is.

The appraisal value of a home will slightly depend on the state of the current home market and the sale of homes similar in the area, but it is largely based on the state of the home itself.

During an appraisal, the buyer or seller doesn't need to be present. The appraiser will put together a report for both to see after the appraisal is complete.

An appraiser will look at some of the following:

If your home has older plumbing and electrical systems, this could bring the home's value down. The value will also vary depending on the state of the appliances left in the home for the buyer. Once you have gotten an appraisal and you are working on the funding for a home, you should have an inspection of the home done.

A home inspection will check many of the same places that the appraiser looked at, but while the home appraisal was done to look for the value of the home, the home inspection looks at the safety of the home. If a home fails an inspection, the buyer has the option to request a decrease on the asking price or they can ask that the sellers have the repairs made before the purchase goes through.

During a home inspection, it is not required that the buyer or seller be present. It is rather recommended that the buyer be present in case they have questions about any issues that are found.

A home inspector will look at things like:

The inspector will also identify anything that could be a fire hazard. If there are too many things wrong with a home, the buyer can decide to walk away and not buy the home at all. The inspection would typically be done before the appraisal is completed to give the sellers a chance to right any wrongs.

Home appraisals and home inspections are both important steps in the home-buying process. Once an inspection is complete on the home you have your eye on, contact us at East Coast Appraisal Service and we can get you a free quote on your appraisal.

Home Appraisals

Home appraisals are often required by a lender for the initial purchase or refinancing of a home. Home appraisals are a way to determine the value of the home. A lender will not borrow you more money to purchase a home than it is appraised to be worth.

Though an appraisal is usually required by the lender, the borrower (home buyer) is usually responsible for paying for the appraisal. There are times when the seller could pay for the cost of the appraisal, but that is a deal that needs to be worked out through your real estate agents as it is not typically the seller's responsibility. Home appraisals cost around $300 to $450 so make sure to account for that cost when you are saving to buy a home.

Appraisal Process

To keep it fair, there are regulations in place that require an appraiser to have no connection to the seller and the buyer. This prevents a buyer or seller from having the ability to call in a family member to give a biased appraisal and say that the house is worth more/less than it actually is.

The appraisal value of a home will slightly depend on the state of the current home market and the sale of homes similar in the area, but it is largely based on the state of the home itself.

During an appraisal, the buyer or seller doesn't need to be present. The appraiser will put together a report for both to see after the appraisal is complete.

An appraiser will look at some of the following:

- Floor plan

- Square footage

- Number of bathrooms

- Number of bedrooms

- Age of the home

- Condition of the home

- Acreage

- Plumbing

- Electrical

If your home has older plumbing and electrical systems, this could bring the home's value down. The value will also vary depending on the state of the appliances left in the home for the buyer. Once you have gotten an appraisal and you are working on the funding for a home, you should have an inspection of the home done.

Home Inspections

A home inspection will check many of the same places that the appraiser looked at, but while the home appraisal was done to look for the value of the home, the home inspection looks at the safety of the home. If a home fails an inspection, the buyer has the option to request a decrease on the asking price or they can ask that the sellers have the repairs made before the purchase goes through.

During a home inspection, it is not required that the buyer or seller be present. It is rather recommended that the buyer be present in case they have questions about any issues that are found.

A home inspector will look at things like:

- Roof

- Stairs

- Siding

- Plumbing

- Electrical

- HVAC

- Foundation

The inspector will also identify anything that could be a fire hazard. If there are too many things wrong with a home, the buyer can decide to walk away and not buy the home at all. The inspection would typically be done before the appraisal is completed to give the sellers a chance to right any wrongs.

Home appraisals and home inspections are both important steps in the home-buying process. Once an inspection is complete on the home you have your eye on, contact us at East Coast Appraisal Service and we can get you a free quote on your appraisal.

When settling an estate in New York, real estate is often the most valuable and complex asset to handle. A professionally prepared appraisal by a certified appraiser is not an optional extra — it’s a critical document that protects executors, beneficiaries, and the estate itself.

Need a real estate appraiser Manhattan NY for inherited property? East Coast Appraisal Service offers certified estate appraisals. Call today.

Understand how residential appraisals handle square footage in Manhattan, NY. East Coast Appraisal Service offers certified appraisal services. Call today.

When someone inherits property—whether it’s real estate, stocks, or other assets—one of the most important (and often overlooked) tax concepts is the “step-up in basis.” An IRS step-up appraisal is the process used to determine the fair market value of an asset at the time of the original owner’s death. That value becomes the new tax basis for the heir. Understanding how this works can save—or cost—significant money when the asset is eventually sold. What Does “Step-Up in Basis” Mean? “Basis” is essentially what an asset is worth for tax purposes. Normally, if you buy something, your basis is what you paid for it. But when you inherit property, the IRS allows that basis to be “stepped up” to the asset’s fair market value as of the date of death. Example: A parent buys a home for $100,000 decades ago At the time of their passing, the home is worth $700,000 The heir’s new basis becomes $700,000—not $100,000 If the heir sells the home for $710,000, they only pay capital gains tax on $10,000—not $610,000. That’s the power of the step-up. What Is an IRS Step-Up Appraisal? An IRS step-up appraisal is a formal valuation that establishes the fair market value of an inherited asset as of a specific date—usually the date of death. For real estate, this means a licensed appraiser evaluates: Comparable sales (comps) Property condition Market trends at that time Location and unique characteristics The result is a retrospective appraisal , meaning it determines value as of a past date, not the current market. Why Is It Important? A step-up appraisal is critical for several reasons: 1. Reduces Capital Gains Taxes Without a proper appraisal, the IRS may assume a lower basis, increasing taxable gains when the asset is sold. 2. Provides Documentation If the IRS ever questions the reported value, a professional appraisal serves as defensible evidence. 3. Helps with Estate Planning and Reporting Executors and heirs need accurate values for estate filings and distribution decisions. When Do You Need One? You typically need a step-up appraisal when: You inherit real estate and plan to sell it The estate did not already establish a value for tax purposes Significant time has passed since the date of death There’s potential for IRS scrutiny (high-value assets) Even if you don’t plan to sell immediately, getting the appraisal early can prevent headaches later. Date of Death vs. Alternate Valuation Date Most step-up appraisals use the date of death as the valuation date. However, in some cases, the estate may elect an alternate valuation date (six months later), if it reduces estate taxes. This decision is usually made by the estate’s executor in consultation with tax professionals. What Makes a Good Step-Up Appraisal? Not all appraisals are equal—especially when dealing with the IRS. A reliable step-up appraisal should: Be completed by a state-licensed or certified appraiser Follow Uniform Standards of Professional Appraisal Practice (USPAP) Clearly state it is a retrospective appraisal Include strong comparable sales data from the relevant time period Be well-documented and defensible Common Mistakes to Avoid Using current market value instead of date-of-death value Relying on informal estimates (like Zillow) Waiting too long to gather historical data Failing to get an appraisal at all These missteps can lead to disputes or higher taxes. Final Thoughts An IRS step-up appraisal might not be the first thing on your mind after inheriting property, but it plays a major role in determining future tax liability. Getting it right can mean the difference between a manageable tax bill and a costly surprise. If you’ve inherited property—or expect to—it’s worth consulting with a qualified appraiser and tax advisor early in the process. A little diligence upfront can protect you financially down the road.

Inherited NYC property? Learn what an IRS step-up appraisal is, why date-of-death value matters, and how NY estate tax works — from a Brooklyn appraisal firm.

ACRIS is NYC's free property records database. Learn what it is, how to look up who owns a property in New York, and what it costs — from a Brooklyn appraisal firm.

Discover why a real estate appraisal in Manhattan, NY, matters with East Coast Appraisal Service. Call 718-834-1700 or click here to learn more.

Get an accurate real estate appraisal in Manhattan, NY from East Coast Appraisal Service. Call 718-834-1700 today to schedule.

Call East Coast Appraisal Service at 718-834-1700 to prepare your home for a professional appraisal with a trusted real estate appraiser in Manhattan, NY.